The start of a new year always brings a fresh perspective and an opportunity to refine your financial strategies. For 2025, several key updates to savings limits, tax rules, and financial planning tools are set to impact your money management. Whether you’re saving for retirement, building an emergency fund, or optimizing tax-advantaged accounts, staying informed is crucial to making the most of what’s available. Let’s dive into the most significant changes and how they can help you achieve your financial goals.

One of the most popular retirement savings tools, the 401k, is getting a boost in contribution limits for 2025. The new annual contribution limit is now $23,500 for both traditional and Roth 401k accounts, up from last year. If you’re over 50, you can add a catch-up contribution of $7,500, bringing your total to $31,000.

For those aged 60 to 63, there’s even better news. A new rule allows an enhanced catch-up contribution of $11,250 during these years. This unique provision is aimed at helping those nearing retirement maximize their savings in a short time frame. If you fall into this age bracket, it’s a great opportunity to supercharge your retirement nest egg.

What You Should Do:

Review your 401k contributions and adjust them to take full advantage of the new limits.

If you’re 60 to 63, ensure you’re making the enhanced catch-up contributions.

Talk to a CERTIFIED FINANCIAL PLANNER® to confirm you’re optimizing these contributions for your long-term goals.

2. IRA Adjustments: Tailored for Your Needs

Individual Retirement Accounts (IRAs) also come with updated contribution limits. For both traditional and Roth IRAs, the 2025 limit is $7,000. If you’re 50 or older, you can contribute an additional $1,000.

However, there are income thresholds to keep in mind. If you’re a high earner—making over $150,000 as a single filer or $236,000 as a joint filer—you may not qualify to contribute directly to a Roth IRA. But don’t worry—a backdoor Roth IRA is a viable option for bypassing these restrictions. This strategy involves contributing to a traditional IRA and then converting it to a Roth IRA, provided you meet certain conditions.

What You Should Do:

Check your income eligibility for direct Roth IRA contributions.

If you’re above the income threshold, explore the backdoor Roth IRA option

3. HSA Limits: Health Savings with Tax Perks

Health Savings Accounts (HSAs) are another powerful tool for those with high-deductible health plans. For 2025, the contribution limits have increased to $4,300 for individuals and $8,550 for families. Additionally, if you’re 55 or older, you can contribute an extra $1,000.

HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. Unlike Flexible Spending Accounts (FSAs), HSAs don’t have a “use it or lose it” policy, making them an excellent long-term savings vehicle for healthcare costs in retirement.

What You Should Do:

Maximize your HSA contributions to take full advantage of the tax benefits.

If you’re married and over 55, ensure both spouses contribute separately to get the catch-up benefit.

Consider investing your HSA funds to grow your balance for future medical expenses.

4. Tax Cuts and Jobs Act (TCJA) Expiration: What to Watch For

One of the biggest questions for 2025 is the potential expiration of the Tax Cuts and Jobs Act (TCJA). This legislation, enacted in 2017, reduced individual income tax rates and adjusted brackets. Unless Congress takes action, these provisions are set to expire, which could lead to higher tax rates for many Americans.

While there’s speculation that some or all of these changes might be extended or made permanent, it’s essential to prepare for any potential tax shifts.

What You Should Do:

Monitor updates on tax legislation and how changes might affect your tax bracket.

Consider strategies like Roth conversions to lock in current lower tax rates.

Work with a tax professional to optimize your tax planning for 2025 and beyond.

5. Volatility and Market Trends: Staying the Course

As with any year, 2025 will likely bring its share of market volatility. While it can be tempting to react emotionally to market swings, maintaining a disciplined approach to your investments is critical for long-term success.

What You Should Do:

Diversify your portfolio to minimize risk and capture growth opportunities.

Rebalance your portfolio periodically to align with your goals and risk tolerance.

Stay informed but avoid making impulsive decisions based on short-term market movements.

6. Holistic Financial Planning: A Must for 2025

Beyond the numbers, effective financial planning involves aligning your money with your life goals. Whether it’s saving for retirement, funding a child’s education, or building generational wealth, taking a holistic approach ensures that all pieces of your financial puzzle fit together.

The beginning of a new year is the perfect time to revisit your financial plan and take advantage of the opportunities available. With higher contribution limits, evolving tax laws, and the potential for market shifts, staying proactive is the key to success.

By understanding the updates for 2025 and implementing thoughtful strategies, you can set yourself up for a prosperous year and a secure financial future. Here’s to making 2025 your best year yet—financially and beyond!

Today we are diving into a question that doesn’t come up as often as it should: How do I personally invest? This is a crucial question that any prospective client should ask. Are you curious what is inside your CFPs portfolio?

I firmly believe that transparency is the foundation of a trustworthy advisor-client relationship. The investments I recommend to my clients are the same ones I would consider for my own portfolio. This principle stems from a straightforward idea: if I am advising on an investment, it should be a good enough investment for my money.

However, investing one’s own money in the same assets recommended to clients requires careful navigation of compliance and regulatory frameworks. These measures exist to protect investors from unethical practices like “front-running,” where unscrupulous advisors manipulate stock prices to their advantage at the expense of their clients. While these regulations add a layer of complexity, they are essential for maintaining trust and integrity in the financial industry. Regardless, a CFPs portfolio should be transparent.

The Core of My Investment Philosophy

At the heart of my investment philosophy is the belief in asset allocation and diversification. It’s a strategy that aligns with the needs and goals of my clients, and it’s the same approach I apply to my own portfolio. Here’s how I break it down:

Asset Allocation and Diversification

I advocate for a well-diversified portfolio as a cornerstone of a sound investment strategy. This involves spreading investments across various asset classes to mitigate risk and capture opportunities in different market environments. For my clients, I develop customized models—equity and fixed-income models—that consider their risk tolerance, time horizon, and specific goals.

For instance, some clients may prefer a heavier weighting in equities for higher growth potential, while others might opt for a more conservative approach with a focus on fixed income. My own portfolio is similarly tailored, reflecting my unique preferences and risk profile. The underlying investments might be consistent across portfolios, but the allocation percentages vary according to individual needs.

The Role of Cash

Cash is an integral component of any investment strategy. I aim to ensure my money is always working for me, and I advise my clients to do the same. With interest rates currently favorable, options like money market accounts, treasury bills, and CDs offer attractive returns with minimal risk. While these conditions may change as the Federal Reserve adjusts its policies, having cash reserves that generate returns is a prudent approach, as should be part of any CFPs portfolio. .

The Fun Side of Investing: Asymmetric Risk

Beyond the traditional asset allocation model, I incorporate a “fun” element into my portfolio—investments characterized by asymmetric risk. This strategy involves committing a small portion of capital to opportunities with significant upside potential but manageable downside risk. It’s a calculated risk that can lead to substantial rewards without jeopardizing financial stability.

Real Estate Investments

Real estate is a key area where I apply this principle. Whether through direct ownership, private placements, or limited partnerships, real estate investments offer a tangible and potentially lucrative investment avenue. However, the critical factor is ensuring the investment generates positive cash flow from the start. It’s essential to avoid properties that drain resources monthly, banking solely on long-term appreciation. Cash flow is vital for managing unforeseen expenses and mitigating risks.

Cryptocurrencies

Cryptocurrencies, particularly Bitcoin, also feature in my investment portfolio. I believe in the underlying technology and the potential future of digital currencies. Despite the volatility and skepticism surrounding crypto, I see it as a valuable addition to a diversified investment strategy. Engaging in this space requires an open mind and a willingness to understand the intricacies of blockchain technology.

Art and Collectibles

Art and collectibles offer another avenue for asymmetric risk investments. The art market can be lucrative, with opportunities to own fractional shares in masterpieces by renowned artists like Jackson Pollock, Van Gogh, or Banksy. While not everyone can afford a multi-million-dollar painting, platforms exist that democratize art ownership. Whether it’s art, collectible cars, or fine wines, these investments provide a fun investment for a passionate investor and the potential for financial gain.

Maintaining a Balanced CFP Portfolio

Despite the allure of high-risk, high-reward investments, the bulk of my portfolio as a CFP remains in more traditional, “vanilla” investments. This conservative approach ensures a stable financial foundation while allowing room for growth. Here are some core principles I follow:

Diversification: Spread investments across different asset classes to minimize risk.

Risk Management: Ensure risky investments are limited to a small portion of the portfolio.

Regular Review: Continuously assess and adjust the portfolio as circumstances and markets change.

Financial Goals Alignment: Keep investments aligned with long-term financial objectives.

Adapting to Change

As an investor, it’s crucial to stay informed and adaptable when it comes to an investment portfolio. Markets evolve, new investment opportunities arise, and personal circumstances change. Regularly reviewing and adjusting the portfolio ensures it remains aligned with current goals and market conditions.

My approach emphasizes flexibility and resilience, allowing for strategic adjustments without losing sight of the core investment principles. This adaptability is crucial, particularly in a rapidly changing financial landscape.

Conclusion

There you have it, a backstage look into a CFPs portfolio. My investment strategy combines traditional asset allocation with innovative, risk-managed opportunities. By aligning my investments with those of my clients, I ensure transparency and shared interests. Whether exploring the potential of cryptocurrencies, the tangible value of real estate, or the fun of art and collectibles, my approach remains grounded in diversification and risk management.

For those interested in exploring these strategies further, I invite you to connect with us!

Retirement planning isn’t just about saving; it’s about mastering the rules of the game. If you’re a high-flyer working for a major airline, you’ve probably heard about the 401(a) and 415(c) limits – but do you truly understand how they can help supercharge your retirement savings? Let’s break down these limits, unravel the intricacies, and set you on the path to maximizing your retirement nest egg.

What is the 401(a) limit?

The 401(a) limit caps the amount of money your employer can contribute to your 401(k), as described by a salary limit. Check here for current year limits. This means when your employer is contributing to your 401(k), they are going to contribute XX% of your salary up to the IRS limit.

For example in 2024, if United contributed 16% of your salary into your 401(k), the most they will add is $55,200 ($345,000 X 16%). If your salary is higher than $345,000, they can no longer contribute to your 401(k), and this is where the money may spill over.

Some more senior pilots may have a salary higher than the salary limit. In this case, they will get the maximum amount allowed from their employer. If your salary is under that, you don’t have to worry about that limit. However, both pilots will have to pay attention to the next limit, called the 415(c) limit, which will limit what you and your employer contribute as a total limit.

401(a) Limit: Your Key to More Employer Contributions

The 401(a)(17) compensation limit, nestled within the U.S. Internal Revenue Code, is your golden ticket to getting your employer to pump more money into your 401(k). This limit caps the portion of your earnings that counts when determining contributions to specific retirement plans, including beloved options like 401(k)s and defined benefit pension plans.

Now, the real magic happens when you align your contributions with the 401(a) limit. This strategic move can lead to a larger employer contribution to your 401(k), leaving you with more take-home dollars. The aim is to maximize your 401(k) without hitting the cap too soon or spilling over.

415(c) Limit: The Sibling of 401(a)

But wait, there’s more! The 415(c) limit, or Section 415(c) limit, is another player in this retirement savings game. This provision in the tax code sets the annual ceiling on contributions or benefits allocated to an individual’s retirement account within qualified plans, spanning 401(k)s, 403(b)s, and pensions.

These limits aren’t etched in stone; they evolve yearly to keep up with inflation and economic shifts. For the most current numbers, consult the IRS or your trusted tax advisor when making retirement contributions.

Making Sense of 415(c): Real-Life Scenarios

Let’s dive into real-life scenarios. Imagine you’ve maxed your contribution (based on 2024 numbers- Check here for current year limits.) at $22,500. Your employer can contribute up to $43,500. If your salary is $280,000 and your company matches 16%, that’s a generous $44,800 from your employer. However, there’s a $1,300 spillover due to the 415(c) limit. In this case, you could reduce your contribution to $21,200 and still receive the full $44,800 employer contribution, reaching a total of $66,000.

Now, what if you’re 50 or older and want to hit the max of $73,500, including a $7,500 catch-up contribution?

401(a) at Play: Maximize Your Employer’s Share

Here’s a twist – you can contribute only the catch-up amount to your 401(k) if your employer’s contributions have already filled your account to the max. Say you earn $345,000, and your employer contributes 16%, giving you $55,200. If you’re under 50, you can add $13,200 to reach the $66,000 cap. If you’re 50 or older, it’s an extra $20,700 to hit the $73,500 limit. Fascinatingly, neither scenario requires you to max out your employee limit of $22,500 plus a $7,500 catch-up.

Crunching the Numbers for Your Benefit

To make the most of these limits, a little number-crunching and projection are in order. Consider your salary history and estimate future earnings to create a strategy that maximizes both your contributions and those from your employer.

Why does all this matter? Because it’s your gateway to getting more money into your 401(k), rather than spillover accounts. And the more you get in now, the better your financial future will look in retirement.

Beyond 401(k) – The Backdoor Roth Conversion

But our journey doesn’t end here. For our high-earning clients in the airline industry, we’re here to uncover your financial dreams and set you on the right track. One exciting strategy to explore is the Backdoor Roth Conversion. This allows you and your spouse to stash away even more, in addition to your 401(k) contributions. It’s a powerful way to build a pool of tax-free retirement dollars.

In a Nutshell

In real-life scenarios, these 401(a) and 415(c) limits offer opportunities for fine-tuning your contributions. By making thoughtful adjustments to your contributions, you can leverage your employer’s contributions and, if you’re 50 or older, take advantage of catch-up contributions. Ultimately, these limits are the building blocks of a more secure financial future in retirement. The more you invest wisely within these boundaries, the more comfortable and stable your retirement years will become. So, remember, it’s not just about accumulating savings; it’s about understanding and utilizing these financial limits to secure your financial well-being in retirement.

What We Can Do for You

As a Certified Financial Planner and Fiduciary Financial Planner, we’ve partnered with over 50 pilots just like you, helping them discover their financial goals and chart a course to success. We can help you navigate 401(a) and 415(c) limits. Those who work with advisors or have done so in the past often have at least double the retirement savings of their peers, sometimes even more. Your financial future deserves expert guidance – let us help you soar towards your retirement dreams.

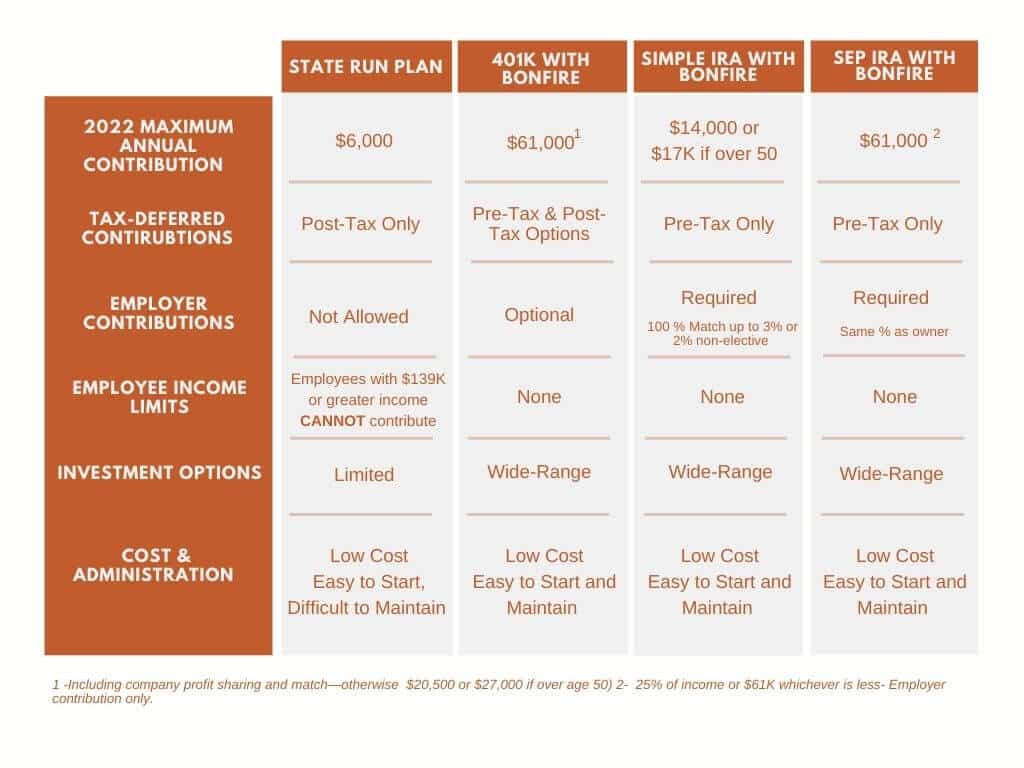

What business owners need to know about Colorado Secure Savings Act

In 2020 Colorado passed the Colorado Secure Savings Program. This law mandates that small business owners enroll in a state-run retirement savings plan. The pilot program launched in October 2022 and employers throughout Colorado are now required to comply.

The purpose of this mandate is to increase access to retirement savings for workers in Colorado. The Colorado Secure Savings Act mandates that qualifying employers provide an employer-sponsored individual plan. The cost of this program will be funded through auto payroll deductions.

In general, this seems like it will have positive benefits for employees. However, it may create additional burdens for employers and may in fact limit employees’ options. Here is what small business owners need to know about the Colorado Mandated Small Business Retirement Plan.

Who needs to comply:

The Colorado General Assembly states that you, as an employer, will be required to implement this program if:

You have five or more employees

Have been in business for two or more years

Don’t have an existing qualifying plan

Companies already offering 401ks or other qualified savings plans are not required to use the Colorado Secure Savings Program. The law states that employers with less than 5 employees or who have not yet been in business for 2 years will not be required to participate. However, they will have the option to offer the program to their employees.

What needs to be done:

While there is limited guidance at the moment from the State of Colorado, employers will be required to offer auto-enrollment and facilitate payroll deductions into the program.

Upon enrollment, employees will opt into the default savings rate for Colorado Secure Savings, which is 5% of their gross pay. Beyond this, deferral rates may vary depending on how much you want to save each year. In addition, age, marital status, and income play a role in the amount that employees can contribute.

However, employees will be able to change their contribution amount or opt-out if desired.

As it is written so far, employers will have 14 days to send employees’ contributions to the program administrator. The program oversight will be done by the board of the Colorado Secure Savings Program. The board is currently chaired by the Colorado State Treasurer. This board will be making a process for withholding employees’ wages and remitting withheld amounts into their Colorado Secure Savings account. It’s not yet clear if the program will offer any integrations with payroll providers to facilitate the timely deposit of contributions.

Penalties for noncompliance:

Fines can be costly. For non-compliance, fines will be $100.00 per employee per year and can ratchet up to $5000.00 annually. The compliance period is one year after implementation.

However, they do state they plan to create a grant program to incentivize compliance. Yet no further details have been released. The good news is it’s really easy to comply by setting up a 401k plan or another qualified plan in advance. Keep reading on to find out how.

General Concerns:

There is little to no guarantee of the level of quality or support that will be available to business owners from the state in implementing and managing the Colorado Secure Savings Program. The government has not released any real guidelines. There are some basics, but how is still very undefined.

Further, if a company offers the state-run plan many of their higher income employees will be excluded. Employees with a Modified Adjusted Gross Income of more than $139,000 or $206,000 married filing jointly cannot participate.

As we wait for more details it’s not a bad idea to consider all the various plan options available to you and your company.

State Sponsored vs Employer Sponsored

There are a handful of states that currently have state mandated plans in place. California, Oregon, and New York are a few for instance. State sponsored plans have pros and cons, which business owners should carefully weigh. On one hand, government-mandated plans are generally a cheap solution with few fiduciary implications. On the other, these plans tend to be inflexible, one-size-fits-all. Plus they come with potential government penalties.

State sponsored retirement plans:

Roth IRA Investment structure (after-tax)

The state board selects investments

The plan will “travel with” people if they change jobs or leave the state

Excludes higher income employees

No employer contributions

No federal tax credits for employers

Creates a significant burden for the employer

As an alternative, an employer sponsored 401k or other qualified plans may be a better option than having the state do it for you. A common misconception is that employer sponsored plans are expensive. However, that simply isn’t the case. Many plans are now being tailored for smaller companies. Plus, the IRS gives tax credits to firms with fewer than 100 employees for some ordinary and necessary costs of starting an employer sponsored plan.

Employer Sponsored 401K plans:

Allow an employee to make contributions either before or after-tax, depending on plan options

Wide range of investments at various levels of risk chosen by the employer or by an advisor

Employee may direct their own investments

Higher Annual Salary Deferral Limit

No employee income limits

Allows for employer contributions

Federal tax credits for the employer for start-up and admin costs and employee education

In addition, offering an employer-sponsored plan to your employees may increase your company’s competitiveness in the job market. It could also help you retain valuable staff. Plus, you and other company leaders can participate.

If you work with a payroll services provider, the software can easily and automatically transfer employees’ funds, making the procedure effortless. Additionally, private plans typically come with the support of financial advisors. Moreover, a financial advisor can help regarding plan types and how best to implement them for your business.

Clearly, adding a 401k or other qualified plans to your company’s benefits package has strategic advantages. Yet, by not providing your employees with a retirement plan, you risk having the state impose one.

Do State-Run Plans Even Work?

Time will tell. However, Oregon, the first state to legally mandate a retirement plan, has pretty dismal enrollment numbers. Since its inception in 2018, only 114 thousand workers have enrolled out of a potential of over 1 million total.

Using Oregon again as an example, there are a lot of restrictions. First, the percentage contribution is fixed. Second, the employee’s first $1,000 gets put into a stabilization fund that since its inception has earned 1.52% per annum, or basically 0%, Or less after factoring in inflation. Finally, if and when they have more than $1,000 invested, they must decide between a fund that is a mixture of stocks and bonds and one that is invested entirely with the State Street Equity 500 Index Fund. (03/31/2022)

By comparison, in the private sector, there are multiple low-cost, exchange-traded funds, most of which averaged an annual return of over 10% during the most recent 10 year period. Some would argue that directing employees away from these superior investment products arguably does a disservice to the employees.

Sample Administrative Duties

Further, Oregon has demonstrated what a significant burden the plan can be on employees. Here is a short list of employer duties that Colorado will likely have as well.

Submit an employee census annually

Track eligibility status for all employees

Provide enrollment packets to all employees 30 days after date of hire

Plus, track whether each employee has opted in or out

If an employee doesn’t opt out within 30 days, set up 5% payroll deduction

Manually auto-escalate all employees annually unless they’ve opted out

Repeat auto-enroll process annually for all employees who have opted out

6-month look-back for auto-escalation:

Track if the employee has been participating for 6 months with no auto-escalation

Provide 60-day notice if they do not opt-out again

Hold open enrollment

Auto-enroll anybody who hasn’t been participating for at least 1 year

It’s too early to know whether state-run programs work. After all, Saving for retirement is a marathon, not a sprint. As an employer, it is important to weigh all options.

If you do not already have an existing plan, and you are skeptical about a government-mandated plan, you can always make your own employer-sponsored plan. Bonfire Financial has many 401k, Simple IRA, and SEP IRA options. We provide affordable, hassle-free solutions that will reduce the administrative burden.

Colorado Secure Savings vs Retirement Plan with Bonfire Financial

How can my business establish its own retirement plan?

Above all, retirement plans don’t have to be expensive or difficult to manage. In light of Colorado’s rollout of the Secure Savings Plan, we are offering small business owners and employers a free, no-obligation call with a CERTIFIED FINANCIAL PLANNER™ to help answer all your questions. We can help you create a better, more efficient retirement plan that is tailored to you and your employee’s specific needs. We are local in Colorado Springs and are here to help with all your retirement plan needs.

An individual retirement account (IRA), specifically a Roth IRA, is a great option to save for retirement. One of the significant advantages of a Roth IRA is that, while contributions are not tax-deductible at the time you make them, the distributions can grow tax-free. This differs from a traditional IRA, where contributions may be tax-deductible, but withdrawals are taxed at your income tax rate.

A Roth IRA offers a unique opportunity to invest in an account that allows your contributions and earnings to grow without being taxed upon withdrawal. Over time, this can result in substantial tax-free savings. While you may not achieve the same extraordinary results as some high-profile investors, any amount of tax-free growth can make a significant difference in your financial future. The earlier you start, the more time your contributions have to compound, making a Roth IRA a powerful tool for long-term wealth building.

Many pre-retirees want to find more ways to save for retirement. They also want to make sure they are setting themselves up for a better tax situation when they start taking money out of their accounts.

However, there are several common mistakes we see that cause people major tax issues or nullify their contributions. Below are the most common mistakes we find and how to avoid them

Mistake #1 – Contributing When You Don’t Qualify

The government wants people to save, however, they don’t want them to be able to save too much. As such, you can earn too much to contribute to a Roth IRA. Whether you’re eligible is determined by your modified adjusted gross income. Plus the income limits for Roth IRAs are adjusted periodically by the IRS. As such Roth IRA mistakes can be made.

If you make contributions when you don’t qualify, it’s considered an excess contribution. The IRS will charge a tax penalty on the excess amount for each year it stays in your account.

How to avoid it:

If you’re close to the income limits, one way to avoid the extra tax penalty is to wait until you’re about to file your taxes. Then you can see how much if anything you can contribute. You have until the day your taxes are due to fund a Roth IRA. This way, you avoid making the mistake of contributing more than the allowable maximum. Plus, helps to avoid paying unexpected penalties.

Mistake #2 – Funding more than one Roth IRA

Let’s say you fund a Roth IRA with Bonfire Financial, and also open another Roth IRA at Vanguard, for example, you cannot contribute money to each Roth IRA. If you contribute more than you’re allowed to your Roth IRA, you’ll face the same excise tax penalties on those extra funds.

How to avoid it:

To avoid this problem, be sure to watch and manage the total amount of contributions in all of your Roth IRA accounts. If you do accidentally put in too much, you can make a withdrawal without penalty as long as it is before the tax filing deadline. You also have to withdraw any interest earned.

Mistake #3 – Not Funding your spouse’s Roth IRA

While your contributions to a Roth IRA are limited by the amount of money you’ve earned in a given year, there is an exception. Your spouse! Even if your spouse has no earned income, they can still contribute to their own Roth IRA via the Spousal Roth IRA. You must be legally married and file a joint return to make this work.

How to avoid it:

By using a Spousal IRA, you can double up on your Roth IRA contributions. You can save even more money per year in tax-free dollars if over 50 years old.

Keep in mind that IRAs are individual accounts. As such, a Spousal Roth IRA is not a joint account. Rather, you each have your own IRA—but just one spouse funds them both.

Mistake #4 – Too large of a Roth Conversion

Roth conversions are a good tool to use to make your future earnings tax-free and avoid RMDs in the future. How these conversions work is by moving pre-existing funds in your traditional IRA or traditional 401K into a Roth or Roth 401k. The amount of money that is converted or moved from one account to the other will be taxable at whatever your current income tax bracket is.

One problem that can happen is that if you are close to the next income bracket and you convert funds over to a Roth, some of the conversion could be taxed at a higher rate. It pushes you into the next income bracket. These conversions cannot be reversed. So, if you are not working with an advisor and your tax professional you can inadvertently pay more taxes than you need to.

How to avoid it:

If you have large IRAs or 401k and would like to convert into a Roth, it is best to watch your income brackets and convert an amount of money that would fill your current income tax bracket but not spill over into the next. It is best to use this strategy over multiple years.

Mistake #5 – Not doing a Backdoor Roth

Many of our clients have incomes that are above or well above the Roth IRA income phaseout. Yet they and their spouses are funding their Roth IRA’s fully each year. How?

By using a strategy called the Backdoor Roth Conversion. A Backdoor Roth Conversion is done by funding an empty IRA then immediately converting the IRA dollars into the Roth IRA. In this way, you are funding a traditional IRA and not deducting from your income, also known as a nondeductible IRA contribution, and then converting into the Roth IRA, which is allowed regardless of income. In this strategy, you indirectly fund the Roth IRA and can continue to do this every year going forward.

How to avoid it:

If you make too much money to contribute directly to a Roth IRA, consider doing a Backdoor Roth. There are some drawbacks to converting a traditional IRA to a Roth IRA. Since the money you put into your traditional IRA was pre-tax, you’ll need to pay income tax on it when you do the conversion. It’s possible that this additional income could even bump you up into a higher tax bracket. We highly recommend talking to a CERTIFIED FINANCIAL PLANNER™ about implementing this strategy.

Mistake #6 – Doing a Backdoor Roth with Money in an IRA

One mistake we often see is someone funding a Backdoor Roth IRA while concurrently having pre-tax dollars in other IRA accounts. The reason this is a problem is that the IRS looks at all accounts. And due to the “Pro-rata Rule” treats them as one. You cannot simply just choose to move after-tax dollars into a Roth IRA.

You have to calculate the amount of money that can be moved into a Roth without paying taxes by dividing the amount of after-tax dollars by the total amount of money in all your IRA accounts.

How to avoid it:

A way to avoid this common pitfall is to account for all IRAs. (SEP IRAs, Simple IRAs, and or traditional IRAs)This will help know whether you can contribute without triggering the Pro-rata rule. You could also convert all pre-tax dollars at once. Or, another option would be to roll your IRA money into a 401k so that you no longer have any money in an IRA.

Mistake #7 -Not properly investing the money

One common mistake we see investors make is that they believe the Roth IRA is an investment when it is simply an account. Just because you contribute to a Roth IRA doesn’t mean it is invested automatically.

It is not enough just to open an account. You have to go into the account and select investments and manage them. If you just contribute to a Roth IRA without selecting an investment in the account, it could be just sitting in cash!

How to avoid it:

Invest the money in your Roth IRA. If you are unsure of a good investment strategy, schedule a meeting with one of our CERTIFIED FINANCIAL PLANNER™ professionals. We can help make sure your Roth IRA is invested correctly for you based on your goals, time horizon, and risk tolerance.

Mistake #8 -Not optimizing your Roth Dollars

Oftentimes, we see Roth IRA investors using allocations that are very conservative. Or they match other allocations in their 401(k). This is a massive oversight and not planning for a proper tax allocation strategy. A Roth IRA should be managed more aggressively than your other accounts so that you can take full advantage of the tax-free benefit.

How to avoid it:

Leave the conservative allocation to the after-tax and tax-deferred accounts. A Roth IRA should be as aggressive as you are willing and capable of doing. One advantage of IRAs over 401k plans is that, while most 401k plans have limited investment options, IRAs offer the opportunity to put your money in many types of stocks and other investments.

Mistake #9 – Forgetting to name Beneficiaries

It’s important to name a primary and contingent beneficiary for your IRA accounts. Otherwise, if something happens to you, your estate will have to go through probate. And that can take more time, cost more money, and cause a lot of inconveniences.

How to avoid it:

Name your beneficiaries and be sure to review them periodically and make any changes or updates. This is especially important in the case of divorce. We see a lot of issues arise because a divorce decree won’t prevent a former spouse from getting your assets if he or she is still listed as a beneficiary on those assets.

Mistake #10 -Not having a CFP® Manage your investment and tax strategy

There are many nuances to opening and maintaining a Roth IRA. The investments, the tax strategies, and the timing of contributions can all make or break your account’s tax-free status. This potentially could cost you additional taxes and penalties.

How to avoid it

Work with a CERTIFIED FINANCIAL PLANNER™ to help you set up, and maintain your Roth IRA. They can help plan for an effective retirement and tax strategy. Having a professional help you with your retirement accounts and other complicated retirement plan strategies can potentially help you avoid expensive Roth IRA mistakes.

To Sum it Up- Don’t make these Common Roth IRA Mistakes

Roth IRAs can provide a lot of great retirement benefits, but they can also be complicated. There are a lot of common mistakes with a Roth IRA. It is important to pay attention to all the regulations and rules to help you avoid these common mistakes.

Have questions about your Roth IRA? Give us a call! We are local in Colorado Springs but help clients all over the nation. We are happy to help.

If you just wrote a big check to the IRS, you may be wondering how you can prepare now to cut your taxes next April. We’ve got you covered. Luckily, there are several legal ways to reduce the amount of tax you pay each year that don’t just include adjusting your withholding. Here are 10, practical and actionable, ways to help you cut your next tax bill and those in the future.

1. UTILIZE YOUR RMD FOR YOUR CHARITABLE GIVING

If you are 73 or older, donating your Required Minim Distribution (RMD) to a qualified charity is a great way to reduce your tax burden. These donations are considered a qualified charitable distribution (QCD) and will not be taxed up to $100,000 per account owner.

A qualified charitable distribution can satisfy all or part of the amount of your RMD from your IRA. For example, if your required minimum distribution was $10,000, and you made a $5,000 qualified charitable distribution, you would only have to withdraw another $5,000 to satisfy your required minimum distribution.

The more you donate in this way, the more you can exclude and cut from your taxable income This is extremely helpful since RMDs are ordinary taxable income that will often push retirees into a higher tax bracket.

Qualified charitable donations are a great way to use up your RMD if you are planning to give to charity. However, keep in mind that it must be a check sent directly from an IRA to the charity.

Schwab allows you to have a checkbook on your IRA that allows you to write such checks directly from your IRA. Be aware, that all donations need to be sent/cashed by 12/31 of the tax filing year.

QCDs can offer big tax savings, as tax rates on regular income are usually the highest. Regardless of the tax benefits, designating this income for charity is a great way to begin or expand your giving and support the causes you care most about.

2. TAKE ADVANTAGE OF TAX LOST HARVESTING

There is always a silver lining, right? For market downturns, that silver lining is tax-loss harvesting. With tax-loss harvesting, you can use your loss to cut your tax liability and better position your portfolio going forward.

Here is how it works, in its simplest form:

First, sell an investment that is losing money and underperforming.

Next, use that loss to reduce your taxable capital gains. This can potentially offset up to $3,000 of your ordinary income for the tax year. (Any amount over $3,000 can be carried forward to future tax years to offset income down the road).

Last, reinvest the money from the sale into a different investment that better meets your investment needs and asset-allocation strategy.

This allows you to free up cash for new investments and mitigate a tax consequence.

As with anything tax-related, there are limitations. Please note that tax loss harvesting isn’t useful in retirement accounts because you can’t deduct the losses in a tax-deferred account. Additionally, there are restrictions on using specific types of losses to offset certain gains. A long-term loss would first be applied to a long-term gain. Then, a short-term loss would be applied to a short-term gain. You also must be careful not to violate the IRS rule against buying a “substantially identical” investment within 30 days.

The best way to maximize the value of tax-loss harvesting is to incorporate it into your year-round tax planning and investing strategy. We always recommend talking to a professional about your specific situation.

3. FUND HSA OR FSA

Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) allow pre-tax dollars to be set aside for medical, vision, and dental expenses, thus reducing your overall taxable income. Each has its own benefits.

It grows tax-free (you can invest your contributions and earn interest)

Can be used tax-free for eligible expenses (

Another great thing about an HSA is that you can keep it forever. Funds roll over and never expire. On the other hand, an FSA is a “use or lose it” type of account. However, an FSA is still a good option because it is funded before tax and comes out tax-free. FSA are employer-sponsored so there is often less involved with enrolling and setting up the plan. As such self-employed filers are ineligible to open able to open an FSA.

Both HSAs and FSAs are good options to help cut and reduce your taxable income.

CONTRIBUTE TO A PRE-TAX RETIREMENT ACCOUNT TO CUT TAXES NOW

Contributing to a retirement plan may be one of the simplest ways to slash what you own to the IRS. Whether a 401k or an IRA, (learn the differences here), both offer tax savings.

4. MAX OUT YOUR 401K

If your employer offers a 401(k), maximizing your contributions is an excellent way to save for retirement while reducing your tax burden. To realize benefits on your next tax bill, contribute to a Traditional 401k rather than a Roth 401k.

A Traditional 401(k) allows you to contribute pre-tax dollars, which lowers your taxable income and can significantly decrease your overall tax liability. This type of account provides immediate tax savings, making it a strong choice if your goal is to minimize your current tax bill. While Roth 401(k) contributions grow tax-free, they are made with after-tax dollars and don’t offer the same upfront benefits. Additionally, contributing enough to receive any employer match ensures you’re fully leveraging this valuable opportunity to grow your retirement savings.

5. CONTRIBUTE TO A TRADITIONAL IRA

Additionally, if you are below the income limits, you can also contribute to a Traditional IRA. They are tax-deferred, meaning that you don’t have to pay tax on any interest or other gains the account earns until you withdraw the money. Contributions to a Traditional IRA are often tax-deductible. However, if you do have a 401k or any other employer-sponsored plan, your income will determine how much of your contribution you can deduct.

6. CONSIDER A CASH BALANCE PLAN

If you are a business owner or solopreneur and have a high income, consider a cash balance plan. A Cash Balance plan is a type of retirement plan that allows for a large amount of money to go in tax-deferred and grows tax-deferred. It is a great option for owners looking for larger tax deductions and accelerated retirement savings.

Cash Balance contributions are age-dependent. The older the participant is, the higher the contribution can be. It can be an extra $60k to over $300k (based on age and income ) on top of combined 401k/ profit-sharing contributions.

An attractive feature of a cash balance plan is that the company offering the benefit can take an above-the-line tax deduction on contributions. Above-the-line deductions are great for tax savings because they reduce income dollar for dollar.

CONTRIBUTE TO AN AFTER-TAX RETIREMENT ACCOUNT TO CUT TAXES IN THE FUTURE

While a 401k, Traditional IRA, and Cash Balance Plan can help curb taxes in the near term, we also recommend planning for future tax implications to help you cut your tax bill for years to come. Roth IRAs are retirement accounts that are made up of your AFTER-tax contributions. However, they offer tax-free growth and tax-free withdrawals.

7. GROW TAX-FREE WITH A ROTH IRA

Again, Roth IRA contributions are after-tax, so you can not deduct your contributions. Nevertheless, your distribution will be tax-free and penalty-free at age 59 ½ Something your future self will thank you for! Another benefit is that a Roth IRA isn’t subject to RMD requirements either.

There are definitely some potential tax savings here, especially for those just starting out. It makes sense to pay taxes on the money you contribute now, rather than later, when your tax rate may be higher.

8. CONSIDER A BACKDOOR ROTH

A Backdoor Roth allows people with high incomes to fund a Roth, despite IRS income limits, and reap its tax benefits. Could it be right for you?

In short, you open a traditional IRA, make non-deductible (taxable) contributions to it, then move that Traditional IRA into a Roth IRA and enjoy the tax-free growth.

It is important to note that you can not have any money currently in an IRA, SIMPLE IRA, or SEP-IRA to make this work properly. There are more complexities involved in setting this up, and we recommend talking with a CERTIFIED FINANCIAL PLANNER™.

9. ROTH CONVERSION

A Roth Conversion involves the transfer of existing retirement assets from a traditional, SEP, or SIMPLE IRA, or from a defined-contribution plan such as a 401k, into a Roth IRA.

You’ll have to pay income tax on the money you convert now (at your current tax rate), but you’ll be able to take tax-free withdrawals from the Roth account in the years to come

You can also use market downturns as an opportunity to do a Roth Conversion. If your IRA goes down in value because of market fluctuations, you could convert the account to a Roth. This will allow you to pay a smaller amount of taxes because the account is down in value. Then you’ll have the money in a Roth when the market recovers, which would then be tax-free.

While there is no predicting what the tax brackets and tax rates will be in the future, if taxes go up by the time you retire, converting a traditional IRA and taking the tax hit now rather than later could make sense in the long run.

10. PAY ATTENTION TO THE CALENDAR

Lastly, from a tax perspective, there is a big difference between December 31 and January 1st. While some things, such as IRA contributions can be made up until the filing deadline, many must be done during the tax year, like qualified charitable distribution.

It is important to plan as far in advance as possible to help minimize your taxes. We recommend meeting with a tax professional and your financial advisor throughout the year.

The key to lowering your tax bill is to plan ahead and cut your tax liability in a way that makes sense for you. It’s impossible to know what regulations, changes, and updates will go into effect during any given tax season, but rest assured that we’ll be here to help you plan. Schedule a free consultation call with one of our CERTIFIED FINANCIAL PLANNER™ professionals today!

Until then, take these tips to heart and remember that reducing your taxes isn’t an impossible task.

Are your turning 65 soon? Turning 65 is a major milestone and pivotal age for your retirement planning. Not only is this an important age for government programs like Medicare and Social Security, but it’s also a perfect time to check other parts of your financial plan, particularly if you’re about to retire. Here are 6 important things to do as you get closer to your 65th birthday to make sure this year and the many years that follow are amazing! (P.S. Read to the end for a special bonus gift for turning 65!!)

Prepare for Medicare

Consider Long Term Care Insurance

Review your Social Security Benefits

Review Retirement Accounts

Update Estate Planning Documents

Get Tax Breaks

1. Prepare for Medicare

Medicare is the most common form of health care coverage for older Americans. The program has been in existence since 1965 and provides a way for seniors to have their health needs taken care of after they retire from the workforce.

What is Medicare?

Medicare is basically the federal government’s health insurance program for people 65 or older (or younger with disabilities). Medicare is primarily funded by payroll taxes paid by most employees, employers, and people who are self-employed. Funds are paid through the Hospital Insurance Trust Fund held by the U.S. Treasury.

When can I enroll in Medicare?

Starting 3 months before the month you turn 65, you are eligible to enroll in Medicare, you can also sign up during your birthday month and the three months following your 65th birthday. Essentially, you have a seven-month window to sign up for Medicare. Be mindful of your timing and enrollment because Medicare charges several late-enrollment penalties.

What does Medicare cover?

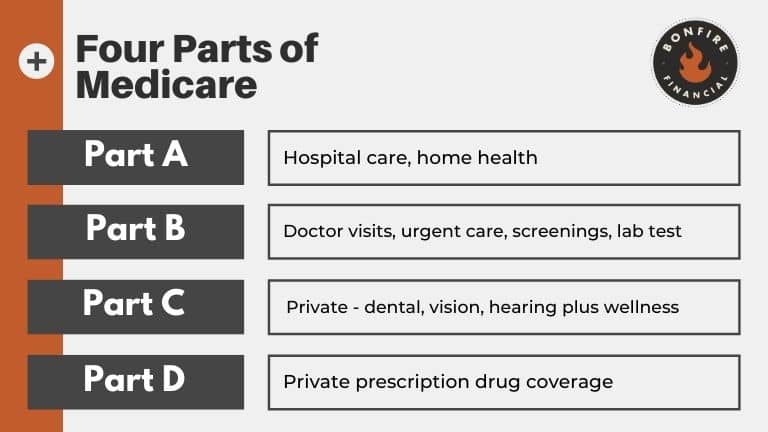

Medicare benefits vary depending on the enrollment plan you choose. Medicare is made up of four enrollment plans: Medicare Part A, Part B, Part C, and Part D.

Here is a quick breakdown of the four parts of Medicare:

Medicare Part A: Know as the Original Medicare, Part A covers inpatient hospital care, home health, nursing, and hospice care. Part A is typically paired with Medicare Part B.

Medicare Part B: Still considered part of the Original Medicare, Part B helps cover doctor’s visits, lab work, diagnostic and preventative care, and mental health. It does not include dental and vision benefits.

Medicare Part C: This option offers traditional Medicare coverage but includes more coverage for routine healthcare that you use every day, routine dental care, vision care, and hearing. Plus, it covers wellness programs and fitness memberships. Medicare Part C is also known as Medicare Advantage and is a form of private insurance. Note that you will not be automatically enrolled in these benefits.

Medicare Part D: Medicare Part D is a stand-alone plan provided through private insurers that covers the costs of prescription drugs. Most people will need Medicare Part D prescription drug coverage. Even if you’re fortunate enough to be in good health now, you may need significant prescription drugs in the future.

While Medicare is great it’s not going to cover all your medical expenses. You’ll still be responsible for co-payments and deductibles just like on your employer’s health plan, and they can add up quickly.

To offset these expenses, a Medicare Supplement (Medigap) insurance policy could be a good option as well. Medigap is offered by private insurance companies and covers such as co-payments, deductibles, and health care if you travel outside the U.S.

How can I enroll in Medicare?

For most people, applying for Medicare is a straightforward process. If you already receive retirement benefits from Social Security or the Railroad Retirement Board, you’ll be signed up automatically for Part A and Part B.

If you aren’t receiving retirement benefits, and you don’t have health coverage through an employer or spouse’s employer, you will need to apply for Medicare during your 7-month enrollment window.

You can sign up for Medicare online, by phone, or in-person at a Social Security office.

Please note that if you have a Health Savings Account (HSA) or health insurance based on current employment, you may want to ask your HR office or insurance company how signing up for Medicare will affect you.

2. Consider Long Term Care Insurance

Another prudent thing to do when you are turning 65 is to consider your long-term care insurance options before retirement.

What is long-term care insurance?

The goal of long-term care is to help you maintain your daily life as you age. It helps to provide care if you are unable to perform daily activities on your own. It can include care in your home, nursing home, or assisted living facility. The need for long-term care may result from unforeseen illnesses, accidents, and other chronic conditions associated with aging.

Medicare often does not provide long-term care coverage, so it is a good idea to factor this additional coverage in.

Why do I need long-term care insurance?

While it may be hard to imagine needing long-term care now, the U.S. Department of Health and Human Services estimates that someone turning age 65 today has almost a 70% chance of needing some type of long-term care service in their lifetime.

Unfortunately, long-term care coverage is often hindsight, only thinking about it once it is needed. Planning for it now can help you access better quality care quickly when you need it and help you and your family avoid costly claims.

How do I get long-term care insurance?

First, talk with a CERTIFIED FINANCIAL PLANNER™ about whether long-term care insurance makes sense for you. Coverage can be complex and expensive. A good Financial Advisor can help guide you to a plan that is right for you.

Most people buy their long-term care insurance through a financial advisor, however, some states offer State Partnership Programs and more employers are offering long-term care as a voluntary benefit.

It is important to start shopping before you would need coverage. While you can’t predict the future, if you wait until you are well into retirement and already having medical issues, you may be turned down or the premiums may be too high to make it a feasible option.

3. Review your Social Security Benefits

If you haven’t yet started to collect Social Security, your 65th birthday is a great time to review your social security strategy to help you maximize your benefits.

When can I take Social Security?

The Social Security Administration (SSA) considers the full retirement age is 66 if you were born from 1943 to 1954. The full retirement age increases gradually if you were born from 1955 to 1960 until it reaches 67. For anyone born in 1960 or later, full retirement benefits are payable at age 67.

In deciding when to start receiving Social Security retirement benefits, you need to consider your personal situation.

How can I maximize my Social Security Benefit?

Turning 65 might raise questions about how to maximize your Social Security befits in retirement. Rightfully so. Receiving benefits early can reduce your payments, however, the flip side is also true. If you’re still working or have savings that will allow you to wait a while on receiving benefits, your eventual payments will be higher. Your benefits can stand to grow 8% a year if you delay until age 70. Plus, cost of living adjustments (COLA) will also be included in that increase.

In addition to delaying receiving your benefits, it is important to make sure all your years of work have been counted. SSA calculates your benefits based on the 35 years in which you earn the most. If you haven’t clocked in 35 years, or the SSA doesn’t have those years recorded, it could hurt you.

Be sure to create a “My Social Security” account and check to make sure your work history is accurately depicted. It is wise to download and check your social security statement annually and update personal information as needed.

Another potential boost in your benefit can come from claiming spousal payments. If you were married for at least 10 years, you can claim Social Security benefits based on an ex-spouse’s work record.

Everyone’s financial situation is different, but it can be helpful to have a plan for how you’re going to approach Social Security before you turn 65.

4. Review Retirement Accounts

Even if you are not planning to retire soon, now (and every quarter for that matter) is a good time to check in on your retirement accounts. Is your portfolio allocated in a way that lines up with your target retirement date? When is the last time you met with your financial advisor? Do you need to catch up a little? Do you have a plan for your Required Minimum Distributions?

Meeting with a CERTIFIED FINANCIAL PLANNER™ can help you evaluate your risk tolerance in comparison to your retirement goals, make sure your investments are aligned to help you retire when you want, and make a plan for you to maintain the lifestyle you want in retirement.

A financial advisor can also help with planning for 401(k) catch-up contributions, RMDs, early withdrawals, or completing a Backdoor Roth.

A big hurdle as retirement approaches is often all the homework you have to do. Penalties, enrollments, coverage gaps, deadlines, etc. A great financial advisor can help guide you through this process.

If you are wondering how to find a great financial advisor, we have put a simple guide here. Or, we would love for you to schedule an appointment now to meet with one of our CERTIFIED FINANCIAL PLANNERs™.

5. Update Estate Planning Documents

The next item on the retirement checklist of important things to do when Turning 65 is to get your estate planning documents and legal ducks in a row. If you do not yet have an estate plan, will, medical directive, or financial power of attorney, it is time to get those in order. It is not too late! If you do have them, take some time to update them.

Have you had recent changes in personal circumstances? Do you need to update beneficiaries? Reviewing your plan at regular intervals, in addition to major life events, will help ensure that your assets and legacy are passed on in accordance with your wishes and that your beneficiaries receive their benefits as smoothly as possible.

Further, it is also a good idea to take inventory and organize all your financial documents. Keep a list of all your accounts (banking and investment), insurance, and estate documents as well as key contact information in a safe place. Make note of any safety deposit boxes you have. Keeping all this info organized and in one place will be a big help to your loved ones during a difficult time.

You’ll feel great knowing that you and your family are prepared

6. Get Tax Breaks

Finally, don’t let Medicare be the only gift to you when you turn 65. Starting in the year you turn 65, you qualify for a larger standard deduction when you file your federal income tax return. You may also qualify for extra state or local tax breaks at age 65.

Many states also offer senior property tax exemptions as well. For example, in Colorado for those who qualify, 50 percent of the first $200,000 of the actual value of the applicant’s primary residence is exempted. Check with your local tax assessor to see what property tax breaks may be available to you.

Turning 65 Birthday Advice

Relax and enjoy it. As much as turning 65 is a time to plan for retirement, it is also a time to celebrate.

If you plan to indulge in a much-deserved tropical getaway or a quick trip to visit your grandchildren, you may be able to take advantage of new travel discounts. Delta, American, and United Airlines all offer senior discounts on selected flights. Additionally, many hotels, car rental companies, and cruise lines all also offer senior discounts. So treat yourself!

Economic downturns often hit the airline industry harder than most. Once again, the airline industry has been grounded by the pandemic and the corresponding economic conditions. As such, layoffs are looming. United Airlines announced it will be laying off thousands of employees, estimated to be 36,000 by October 1, 2020. Additionally, United Airlines said the jobs of more than 14,000 employees are at risk when federal aid expires in the spring of 2021. These layoffs could affect everyone from customer service employees, flight attendants, to pilots. Many other airliners may follow suit.

The fallout from 9/11 and the impact of the 2008 Financial Crisis took the airline industry roughly 2-3 years to recover. It is hard to say how long the coronavirus impact will last or how it will all turn out.

If you are worried you might be one of the airline employees to be laid off or already have been, there are many concerns you may have. From how to pay bills, to how long will this last, to how to keep medical insurance and benefits… the list goes on.

What should I do if I am laid off?

We have put together some tips, ideas, and strategies to help you get through this tough situation.

Covering your living expenses

Being able to cover your living is by far the most important question and concern. There are a number of strategies to help navigate this and there are also some new provisions from the CARES ACT that can help if you are a United Airline employee who has had to face the layoffs.

Your emergency fund

An emergency fund is a savings account or separate account that is set aside for when the unexpected happens, like being laid off. We recommend that our clients have 3-6 months of their monthly expenses saved in this kind of account. The goal is to use this money to pay for your mortgage, food, etc. It is designed to help you bridge the gap of unemployment to your next job or getting rehired when things recover.

One often-overlooked task is once you are employed again to refill your emergency fund. This account can help you in a tough situation but be sure to replenish it to ensure it is there for the next time something unexpected comes up.

If you do not have an emergency fund in place, read on for some other ideas that can help.

Claiming unemployment

If you received a WARN, it is important to start planning ahead now. You can now qualify for weekly unemployment payments from the state in which you worked. Many people fly out of a hub that is different from the state that they live in. When applying for unemployment, use the state that you work out of. Selecting reason for unemployment: “Coronavirus” can streamline the paperwork process. A quick Google search of your state and unemployment will land you on the right page. Look for “.gov” in the address.

Mortgage Forbearance

Mortgage Forbearance means you can postpone your mortgage payment temporarily. For 180 days you can request a forbearance from your mortgage lender. If granted it means you will not have to pay your mortgage for about 6 months. However, this is not mortgage forgiveness. You still owe the full amount and interest still accrues on the months you do not pay. You will need to work out the details and repayment plan with your lender as each situation is different. Per the CARES Act, no additional fees or penalties will be applied if you require forbearance.

Retirement Account Withdrawals

Taking a distribution or withdrawal from your 401(k) should be a last resort. Your 401(k) money is intended to support your retirement. However, with the intensity and impact of the United Airline layoffs caused by COVID-19, the CARES Act has set up many relief options.

Traditionally, you could not access your retirement account before the age of 59 1/2 without having to pay a 10% penalty and income tax. The CARES Act has waived this 10% penalty. Since all retirement accounts (Roths excluded) are funded with pre-tax dollars and the income tax is normally due in the year of a distribution.

The CARES act has allowed distribution in 2020 up to $100,000 be taken out and the taxes are due over the next 3 years. That is much better than having to pay all $90,000 in 2020. The money will come out of your account’s investments pro-rata, so if you have half your money in large-cap stocks and half in small-cap stocks, the money will be sold in them equally to fund the distribution.

401(k) Loan

Taking a loan from your 401(k) is not a good idea because you will be taxed on the distribution, and you will have to repay the loan. There could potentially be many more downsides to taking a loan rather than just distributing the money. If you are furloughed or leave the plan, you will be subjected to a faster repayment schedule.

Taking out a loan from your 401(k) results in taxes on the loan amount. You must also repay the loan using after-tax dollars. Once you repay the 401(k) loan, the IRS will still tax the money again as income when you withdraw it in retirement. This means you face double taxation on the money, rather than being taxed only at distribution.

Miscellaneous Items

Many car manufacturers are offering payment deferrals during this time. If you are unable to make payments comfortably on your car, be sure to reach out to your car’s manufacturer’s finance department to discuss payment options. Many newer cars (2018 or newer) will have more generous payment options than older vehicles.

Also, a voluntary separation could be a good idea if you are close to retirement. The benefits of the United Airlines Retirement Health Account (RHA) can help you pay for medical insurance.

What about my Benefits if I am laid off??

United Airline layoffs are hard enough, luckily you can retain certain benefits. For instance, health insurance, RHA, and you’re retirement accounts can still provide you benefits.

Health Insurance

COBRA is a government bill that lets you keep your medical insurance with your company for up to 3 years. You will have the same coverage and plan, except you will have to pay 100% of the premium (plus a 2% premium for administration costs for a total of 102%) Look at your most recent pay stub to see how much you and your employer were paying for medical insurance.

Retirement Health Account

Your Retirement Health Account (RHA) is a unique account granted directly to United from a private letter ruling with the IRS. The RHA is used to pay for out-of-pocket medical expenses and health insurance premiums when retired, furloughed, or separated from service. The RHA can also be used to pay for your COBRA premiums. Click here for more details on how to use your RHA.

401(k) and Retirement Investments

There are some options you can choose to do with your 401(k) when you have faced a layoff.

You can keep it with the company. Nothing will change as you will have the same investment options and access.

You can withdraw the money, as we mentioned above. However, this is not the best action to take if it can be avoided.

You can roll your money into an IRA. There are no taxes on this move, and it can give you more investment options and control of your money.

Our preference is to roll your 401(k) over into an IRA so that you have better access to your account while avoiding the administration and investment fees from United, Fidelity, or Charles Schwab. We can build you a custom portfolio based on your needs and our custom investment research for a fee typically lower than your Fidelity and Charles Schwab 401(k) options.

Our expertise is working with pilots and aircrew in providing them the best investments through our relationship with Charles Schwab. Leveraging our partnership with Charles Schwab we can build you a custom portfolio in your PCRA.

What’s Next?

We can help you navigate one of the most difficult times the airline industry has ever faced, and that is really saying a lot! We work with many pilots, crew members, and their families and help them prepare for a successful retirement and reach their financial and life goals.

Bonfire Financial is a fiduciary, fee-only, financial advisor. We have a staff of Certified Financial Planners™ that specialize in helping United Airline Employees and Pilots.

As a United Airlines or major airline employee, we would like to offer you a free consultation to help answer any questions you may have and help you get a game plan in place. Schedule your call now.

Whether it is hiring a financial advisor, picking a mutual fund, or refinancing your mortgage it is a good idea to ask a lot of questions when it comes to your money. However, if you only ask a few, here are our top 3 questions to ask before making any financial decision.

What is the investment philosophy?

Make sure to ask yourself if the investment makes sense to you. It may be great for 99% of the population but is it a fit for you and your current situation. Does it match up with your risk tolerance and timeline? Really take the time to contemplate this. Further, do you understand it? Or is it too complex? Understanding this will help move you forward in a meaningful way.

Do I trust the person giving the advice or offering the investment?

Simply put, what is your gut telling you about who is behind this. What is the person’s credibility and credentials? Was it your cousin Eddie spouting off a stock tip at the family reunion? Or a longtime friend and financial advisor who has been in the industry for years? It may seem like a no-brainer to ask this question, but it is sometimes easy to get caught up in the hype of the product and the potential returns.

A quick way to tell if an advisor truly has your best interest in mind is if they are CFP® (Certified Financial Planner)- learn more on thathere, but in short, it means they are a true fiduciary and must have your best interest in mind regardless of commissions. Trust is so important, don’t take it lightly.

What is the downside risk, and can I afford it?

What can you stand to lose? Sure, look at what the potential of the investment is, but don’t ignore the risk. Make sure the amount you invest matches your risk tolerance. The old saying stands true here- “Don’t put all your eggs into one basket.” Before you make an investment decision know the risks.

Short and simple, those are the top 3 questions to ask before making any financial decision!

Are you considering an investment and aren’t sure if it is right for you? Asked these questions and are still unsure? We are here to help…just set up a call.

Managing your finances can be difficult and time-consuming. However, finding someone to handle your finances can be just as challenging. Want a tip to make it easier? Hire A CFP ®.

People often ask us what is a CFP ®, how are they different from other financial advisors, and the reasons to hire a CFP ®. We are going to be breaking all that down for you today.

What Is a CFP® Professional?

First, it’s more than just an acronym. Unlike some designations that are worth little more than the paper they’re printed on, the CFP ® (CERTIFIED FINANCIAL PLANNER™) designation is one of the most esteemed financial certificates around. Each CFP ® is held to an extremely high standard and requires an immense amount of work. Typically nine months to two years of study.

In the US, as of 2025, there are only 101,505 CFPs ® and only 3,150 in the state of Colorado, according to the CFP® Board professional demographics. The exam itself is a grueling 7-hour test that assesses the financial advisor’s ability to apply principles of financial planning. It covers all areas of insurance, investments, income taxes, retirement, estate planning, ethics and conduct, and financial plan development, among many other skills.

Beyond the test, there is so much more that goes into the certification. We have condensed it down to the top 4 Reasons to Hire a CFP®.

4 Reasons to Hire a CFP ®

Fiduciary Standard

Ethics Code

Fitness Standards

Experienced Life-Long Learners

Let’s dive into it:

1. Fiduciary Standard:

Currently, the SEC has NO uniform fiduciary standard that applies to all financial professionals who provide personalized investment advice. This means there is no oversight to protect consumers and clients from paying excessive commissions or receiving substandard performance. Consumers are exposed to even greater and unnecessary risks from products that may be deemed suitable (more on that here) for them but are inferior to other available options and not necessarily in their best interests.

The CFP ® Board has a Code and Fiduciary Standards that require CFP ® professionals to act in the best interest of the client at all times when providing financial advice. So, as a CFP ®, we have a legal requirement to act in your best interest, all the time. In addition to this standard, Bonfire Financial is also a Registered Investment Advisor which furthers this obligation.

2. Ethics Code:

All CFP ® practitioners agree to abide by a strict code of professional conduct, known as CFP ® Board’s Code of Ethics and Professional Responsibility, that sets forth ethical responsibilities to the public and clients. This ensures we act with honesty, integrity, competence, diligence, and offer services objectively.

It’s a pledge to protect the confidentiality of all client information, avoid or disclose and manage conflicts of interest and always act in the client’s best interests.

3. Fitness Standards:

Further, the CFP ® Board has also established specific character and fitness standards for the CFP ® certification. This ensures that an individual’s prior conduct would not reflect adversely upon the profession or the CFP ® certification marks. This helps you know that if you hire a CFP ® you won’t find out later that they have:

A felony conviction for theft, embezzlement, or other financially-based crimes.

A felony conviction for tax fraud or other tax-related crimes.

Revocation of a financial license (e.g. registered securities representative, broker/dealer, insurance, investment advisor).

A felony conviction for any degree of murder or rape.

A conviction for any other violent crime within the last five years.

A felony conviction for non-violent crimes (including perjury) within the last five years.

Personal or business bankruptcies.

4. Experienced Life-Long Learners:

CFP ® professionals are required to complete 3 years of experience related to delivering financial planning services to clients. They also must have a bachelor’s degree prior to earning the right to be a CFP ®. This real-life experience means that CFP ® professionals have practical financial planning knowledge. They can truly help you create a realistic financial plan that fits your individual needs.

Once certified, CFP ® professionals are required to maintain technical competence and fulfill ethical obligations. Every two years, they must complete a minimum of 30 hours of continuing education to stay current with developments in the financial planning profession and better serve clients.

Need more reasons to hire a CFP ®? We’d love to answer any other questions on what it means to have a CFP ® working for you, feel free tocontact us.

At Bonfire Financial we pride ourselves on having a team of CERTIFIED FINANCIAL PLANNERs™ and we can’t wait to help you!

We use cookies to improve and customize your browsing experience and analyze visitor behavior. By continuing to use this site, you consent to our use of cookies. ACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are as essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Thank You For Your Subscription

You’re in! Thanks for subscribing to our monthly newsletter. We will be sending you market updates, financial insights and inspiring travel ideas soon but in the meantime check out our blog, join us on Instagram or pop over to Pinterest.

Your Appointment Request has been Received

Thank you for reaching out! We are excited to learn more about you. Someone from our team will be in touch shortly.

Sign up now

Join us around the fire for monthly market updates, financial insights and inspiring travel ideas.

Client Login

Client Login