Client Login

Client Login

Certificates of Deposit

In the ever-evolving landscape of investment opportunities, some strategies remain steadfast, proving their worth across decades. One such strategy is the use of Certificates of Deposit (CDs). Often overlooked in favor of more glamorous investment options, CDs are now regaining attention due to their stability and attractive returns in the current high-interest-rate environment. Today we are delving into the mechanics of CDs, their benefits, and why they should be considered a valuable component of a well-rounded investment portfolio.

Listen Now:

iTunes | Spotify | iHeartRadio | Amazon Music | Castbox

–

What is a Certificate of Deposit (CD)?

A Certificate of Deposit (CD) is a financial product offered by banks and credit unions that provides a fixed interest rate for a specified term. When you invest in a CD, you are essentially lending your money to the bank for a predetermined period, which can range from a few months to several years. In return, the bank pays you interest at a rate that is typically higher than that of regular savings accounts. At the end of the term, known as the maturity date, you receive your initial investment back along with the accrued interest.

The Mechanics of CDs

CDs operate on a simple premise: you deposit a sum of money for a fixed term, and in exchange, the bank agrees to pay you a fixed interest rate. The key components of a CD include:

- Principal: The initial amount of money you invest.

- Term: The length of time your money is held by the bank, which can range from a few months to several years.

- Interest Rate: The fixed rate at which your money grows during the term.

- Maturity Date: The date on which the term ends and you can withdraw your principal plus interest.

For example, if you invest $10,000 in a one-year CD with an interest rate of 5%, you will earn $500 in interest over the term. At the end of the year, you will receive $10,500.

Benefits of Investing in Certificates of Deposit

1. Stability and Security

One of the primary advantages of Certificates of Deposit is their stability. Unlike stocks or mutual funds, which can fluctuate in value, CDs offer a guaranteed return. This makes them an attractive option for risk-averse investors or those seeking a safe place to park their money during uncertain times. Additionally, CDs are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per depositor, per institution. This means that even if the bank fails, your investment is protected.

2. Predictable Returns

With a fixed interest rate, CDs provide predictable returns. You know exactly how much interest you will earn over the term, allowing you to plan your finances with confidence. This predictability can be especially valuable for retirees or others who rely on their investments for steady income.

3. Higher Interest Rates

CDs typically offer higher interest rates than regular savings accounts. In the current high-interest-rate environment, this difference can be significant. For example, while a savings account might offer an interest rate of 0.5%, a one-year CD might offer 5%. This higher rate can make a substantial difference in your overall returns, especially for larger investments.

4. Protection Against Market Volatility

In times of market volatility, Certificates of Deposit can serve as a safe haven for your money. Unlike stocks or bonds, which can lose value in a downturn, the principal and interest of a CD are guaranteed as long as you hold the CD to maturity. This can provide peace of mind during turbulent economic periods.

Why CDs Are Regaining Popularity

In recent years, CDs have been overshadowed by other investment options due to historically low interest rates. However, as interest rates have risen, CDs have become more attractive. Here are a few reasons why CDs are regaining popularity:

1. Rising Interest Rates

As central banks have raised interest rates to combat inflation, the returns on CDs have become more appealing. Investors can now find CDs offering 5% or more, making them competitive with other fixed-income investments.

2. Low-Risk Environment

With economic uncertainty and market volatility, many investors are seeking low-risk options. CDs provide a secure place to invest money without the risk of loss, making them an attractive choice for conservative investors.

3. Diversification

CDs can be an excellent tool for diversifying an investment portfolio. By including a mix of stocks, bonds, and CDs, investors can balance risk and return, ensuring that a portion of their portfolio remains safe and stable.

4. Liquidity Planning

For those who may need access to their funds at specific times, CDs offer predictable liquidity. By laddering CDs—purchasing multiple CDs with staggered maturity dates—investors can ensure that they have access to cash at regular intervals while still earning higher interest rates.

Considerations When Investing in CDs

While CDs offer many benefits, there are some considerations to keep in mind:

1. Limited Liquidity

When you invest in a CD, your money is tied up for the duration of the term. If you need to access your funds before the maturity date, you may incur early withdrawal penalties, which can eat into your returns. It’s essential to ensure that you won’t need the money before the CD matures.

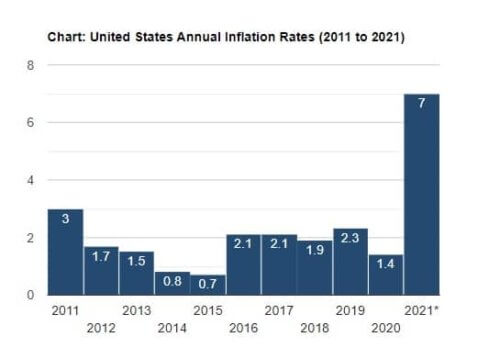

2. Inflation Risk

While CDs provide a fixed return, inflation can erode the purchasing power of your money over time. If inflation rates are higher than the interest rate on your CD, your real return (adjusted for inflation) may be negative. It’s crucial to consider inflation when evaluating the potential returns on a CD.

3. Opportunity Cost

By locking your money into a CD, you may miss out on other investment opportunities that could offer higher returns. It’s essential to balance the security of a CD with the potential for higher returns from other investments.

How to Get Started with CDs

If you’re considering adding CDs to your investment strategy, here are a few steps to get started:

1. Research Interest Rates

Shop around to find the best interest rates on CDs. Different banks and credit unions offer varying rates, so it pays to compare options.

2. Determine Your Investment Amount

Decide how much money you want to invest in CDs. Consider your overall financial goals and how much liquidity you need.

3. Choose Your Term

Select a term that aligns with your financial needs. Shorter terms offer more liquidity but may have lower interest rates, while longer terms lock in higher rates but require you to commit your funds for a more extended period.

4. Ladder Your CDs

Consider laddering your CDs to provide regular access to funds while maximizing your returns. This involves purchasing multiple CDs with different maturity dates.

5. Monitor and Reinvest

Keep an eye on your CDs and their maturity dates. When a CD matures, evaluate the current interest rates and decide whether to reinvest in a new CD or use the funds for other purposes.

Conclusion

In today’s high-interest-rate environment, Certificates of Deposit are once again becoming a valuable tool for investors seeking stability and attractive returns. With their guaranteed interest rates, FDIC insurance, and protection against market volatility, CDs offer a secure investment option for those looking to balance their portfolios. By understanding the mechanics of CDs and considering their benefits and limitations, you can make informed decisions to enhance your financial strategy. Whether you’re a conservative investor or simply looking for a safe place to park your money, CDs deserve a closer look in the modern investment landscape.

Next Steps:

Are you wondering if Certificates of Deposit are right for your specific situation? Feel free to set up a call with us to get personalized advice.